FINTECH OP-ED

Fintech Industry Trends: The Next Phase of Disruption

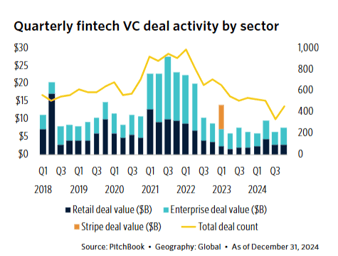

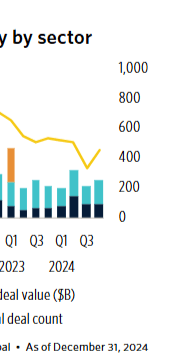

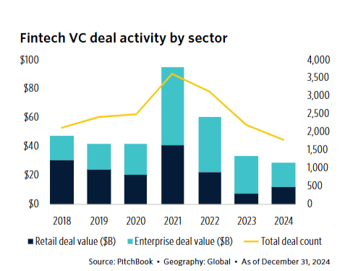

Fintech has been one of the hottest investment sectors over the past decade, but we’re entering a new phase—one that separates hype from real, scalable innovation. The days of easy VC money flowing into every neobank or payments startup are over. The focus is now on profitability, regulatory navigation, and infrastructure plays.

The fintech winners of this next cycle will be those that capitalize on embedded finance, AI-driven underwriting, and the tokenization of real-world assets (RWAs).

1. Embedded Finance: The Invisible Fintech Revolution

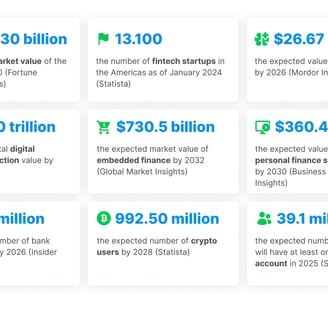

The best fintech products are becoming invisible. Consumers don’t necessarily want a new bank—they want seamless financial tools integrated into the platforms they already use. This is where embedded finance is taking over.

Companies like Shopify, Uber, and even TikTok are turning into fintech players, integrating payments, lending, and banking services directly into their ecosystems. Businesses that used to rely on external financial partners are now monetizing their own financial flows.

For investors, this means fintech infrastructure is where the real opportunity lies. The payment processors, API providers, and compliance enablers facilitating embedded finance will capture more value than standalone consumer fintech apps.

2. AI-Powered Underwriting and Risk Management

AI is fundamentally changing how financial institutions assess risk. From credit underwriting to fraud detection, machine learning models are outperforming traditional scoring methods. This isn’t just about better decision-making—it’s about unlocking entirely new markets of borrowers and financial participants.

The major shift here is in alternative data. Traditional credit scores are becoming less relevant as fintech lenders tap into real-time income data, transaction history, and behavioral analytics. The result? More efficient lending models that can extend capital to underserved markets while minimizing defaults.

For investors, the focus should be on fintech companies leveraging AI for risk assessment rather than just front-end UX improvements. The infrastructure behind smarter lending is where long-term value will be created.

3. The Tokenization of Real-World Assets (RWAs)

The crypto boom may have cooled, but blockchain infrastructure is quietly revolutionizing financial markets through tokenized real-world assets (RWAs). Think private equity shares, real estate, and even government bonds—all becoming tradable on-chain with fractional ownership models.

This isn’t just a DeFi experiment anymore. BlackRock and JPMorgan are actively exploring tokenized fund structures, and central banks are laying the groundwork for regulated digital asset markets. Tokenization has the potential to increase liquidity in historically illiquid assets, making alternative investments more accessible to a broader range of investors.

The opportunity here? Platforms and protocols that facilitate RWA tokenization while ensuring compliance with evolving regulations. The fintech companies that bridge the gap between traditional finance (TradFi) and blockchain-native infrastructure will define the next wave of financial innovation.

Final Thoughts

Fintech is moving past its hype cycle. Neobanks without a path to profitability are struggling, and payment startups that don’t own proprietary infrastructure are losing margin to larger incumbents. The future of fintech belongs to companies that embed financial services seamlessly, leverage AI to reimagine risk, and tokenize real-world value.

The next decade won’t be about disruption for the sake of it—it’ll be about efficiency, compliance, and unlocking new financial markets. Smart capital will follow.